Better lucky than good

How the Trump administration could yet get to a good manufacturing policy

The Trump administration’s embrace of tariffs, far from driving a renaissance of domestic manufacturing, is already harming it. As the administration continues to reverse itself into a more rational trade policy, it will need to look elsewhere for the elements of an effective manufacturing policy. Fortunately, several upcoming opportunities could meaningfully advance American competitiveness.

Manufacturing matters. The failure of US policy has been to conflate three distinct issues—the need to maintain a viable defense industrial base; failure to address anticompetitive foreign behavior and underinvestment in U.S. industrial competitiveness; and inadequacies of the social safety net—into a generalized hostility to trade that is out of step with the wishes and interests of America’s people.

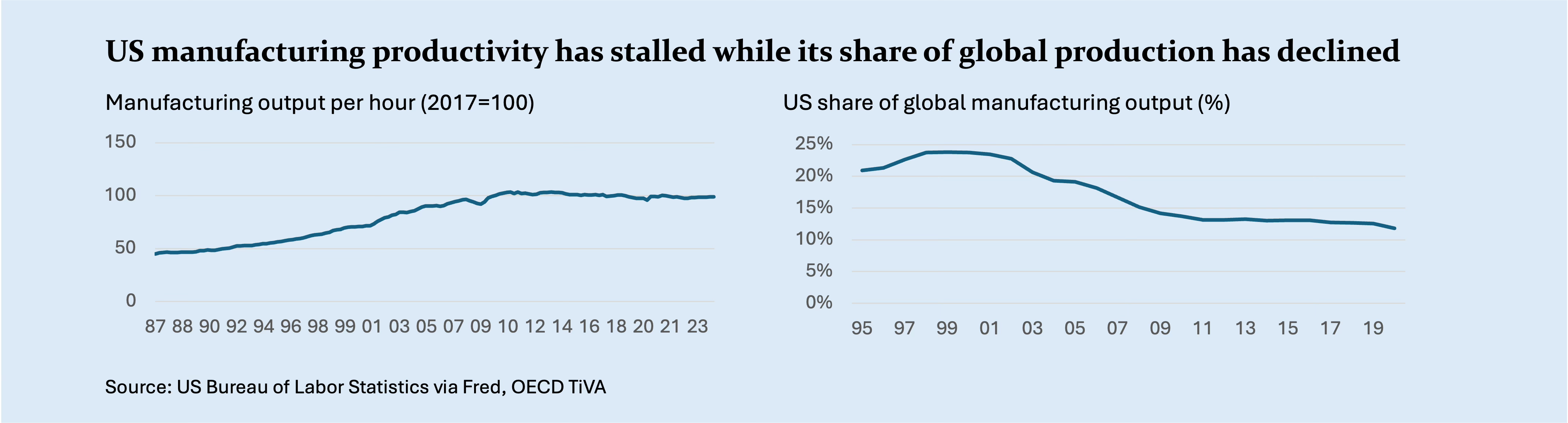

The United States remains the world’s second largest manufacturer and, in many products, continues to lead the world. Since the sector’s 1979 peak of 19.5 million workers, employment has fallen to 12.5 million today. Both China’s emergence as a trading power and improved productivity share responsibility for this decline. This has caused undeniable and largely unaddressed hardship in communities across the country.

But for more than a decade, US manufacturing productivity has stalled, for reasons that escape ready explanation; over that same time period, a new report for the US Chamber of Commerce finds, China has made significant progress in reducing dependencies on the rest of the world and accelerating the country's competitiveness and technological leadership.

America’s manufacturing policy cannot afford to be backwards-looking. It must be focused clearly on what it will take to lead in emerging industries and master new forms of production. It must also recognize that the next generation manufacturing workforce will be smaller and require new skills. Support for those who are dislocated and unable to transition is needed alongside intensive investment and reimagination of the education system to ensure that more do not follow in their wake.

As a goal, the US should seek to bring its share of global manufacturing output (currently around 12%) closer to its share of global GDP (roughly 25%); by 2050, the US share of global GDP could be closer to 16%. Such a target could support several of U.S. Trade Representative Jamieson Greer’s priorities, including boosting manufacturing’s share of GDP and raising median wages. It would also provide a better measure of success than focusing solely on reducing trade deficits.

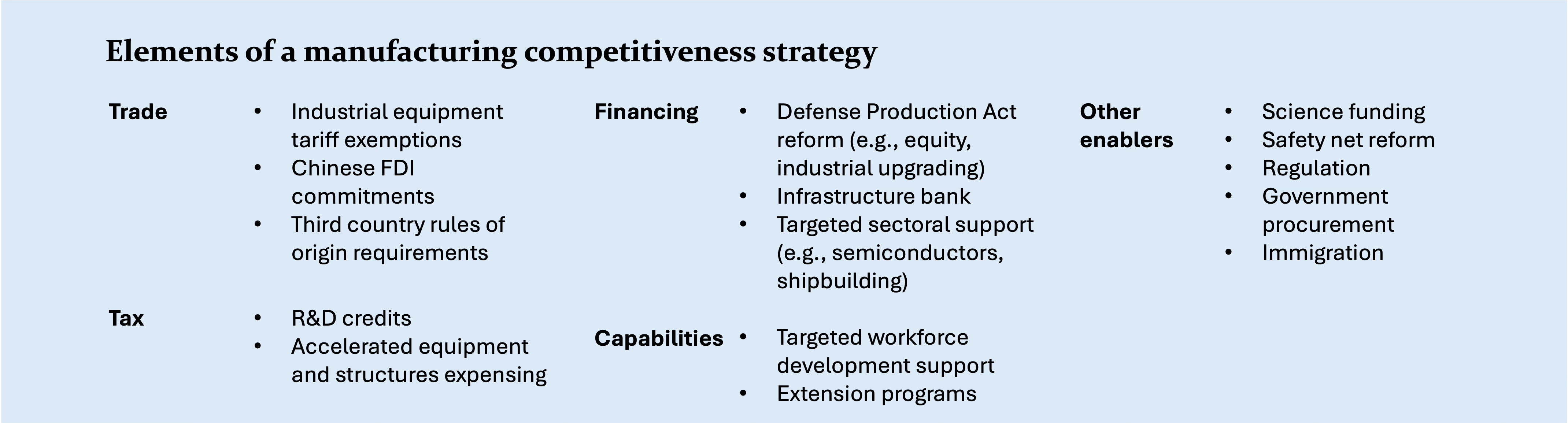

First, do less harm on trade

Higher tariffs are harming domestic manufacturers by raising input costs and lowering demand, particularly as exporters face retaliation from other countries. Uncertainty acts as a further suppressant to demand and investment. Although tariffs on China, in particular, will certainly fall below today’s extreme levels, they are likely to remain elevated on an historical basis. Already, the United States has granted exemptions for select categories of goods, such as electronics, that are both politically salient and difficult to diversify. Similar exemptions are needed for the industrial equipment that the manufacturing sector relies on.

When negotiations with China begin in earnest, President Trump should make good on his expressed openness to Chinese investment. Investment that served as a substitute to imports would more sustainably contribute to a narrowing of the deficit, inject needed capital into America’s industrial base, and accelerate the transfer of know-how from China’s leading firms. Beyond China, the targeted use of rules of origin with third countries can reinforce supply chain diversification. One possible outcome of the administration’s trade negotiations is that the US reaches meaningful agreements with enough individual trade partners that the prospect of signing up to a revised Trans-Pacific Partnership becomes less daunting in a post-Trump administration.

Tax reform: promoting investment and R&D

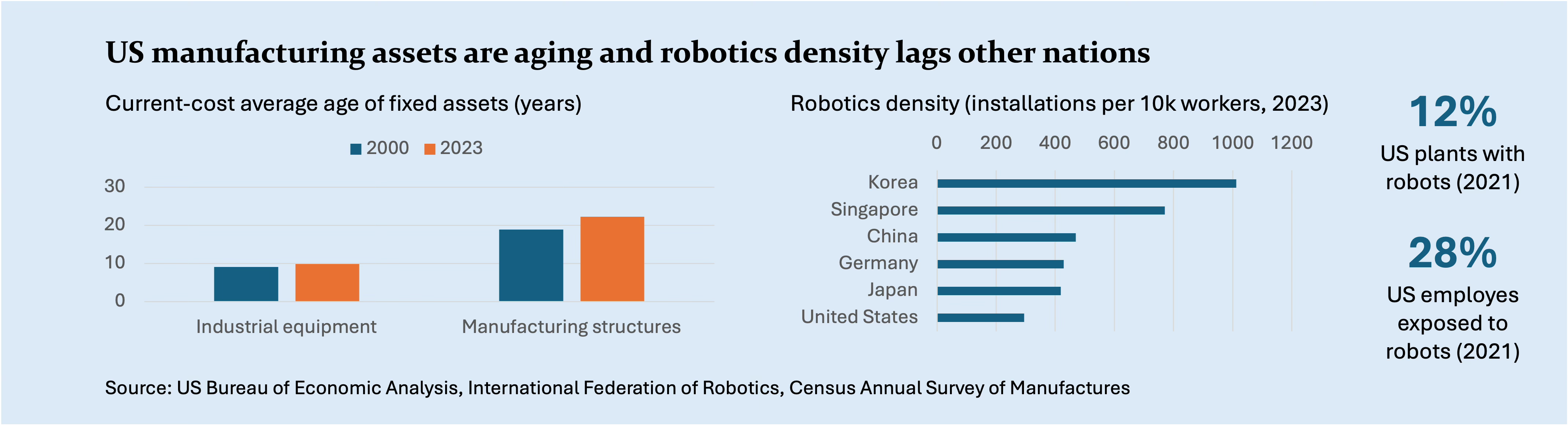

The broader wisdom of America’s fiscal policy notwithstanding, tax incentives that encourage research and development and investment in equipment make sense. Especially welcome are proposals to extend accelerated expensing to include investment in factory construction given that the average age of US factories now exceeds 20 years. McKinsey estimates that traditional manufacturing sectors like autos and chemicals will require additional investment of $250 billion over the next decade to remain competitive. No less challenging will be to increase the share of R&D spending on manufacturing itself: America spends just 3% of its research dollars on better manufacturing, compared to 15% for Germany and 34% for Japan.

Deregulation: an accelerant to growth

Secretary of the Treasury Scott Bessent describes deregulation as the third pillar of the Trump administration’s economic policy, alongside tariffs and tax reform. Streamlining regulation can both reduce compliance costs and induce additional economic activity. A report by the National Association of Manufacturers has estimated that if the US regulatory burden were closer to countries like Switzerland or Denmark, US GDP would be nearly $2 trillion larger.

Defense Production Act

By fall, Congress will need to reauthorize the act that enables the government to address critical industrial capacity needs. Under the DPA, the government can compel production; issue grants, loans, and loan guarantees; and make advance purchase commitments. Proposals for reform have included a higher ceiling on project sizes and allowing a greater share of funds to be carried over. More ambitious reforms are possible. One would be to allow DPA funds to be deployed as equity. Another would be to extend the logic of the Civil Reserve Air Fleet, in which the government contracts with airlines for the right to use their airlift capacity in emergencies, to other domains. One could envision a similar logic for other advanced manufacturing platforms, such as robotics or additive manufacturing infrastructure, supporting the build out of a capital stock that will enhance productivity, competitiveness, and readiness to support defense needs. Loan guarantees to support upgrading America’s capital stock would similarly advance this goal.

Ships Act

Chips are out, ships are in as the American industrial policy priority. Among the administration’s first moves was to impose a fee on Chinese-owned or operated ships. In parallel, Congress is considering a bill that would create a 250-vessel “strategic commercial fleet.” If the legislation advances, Congress should ensure that it includes broader manufacturing competitiveness provisions. Workforce development and expanding extension programs that help small- and mid-size plants embrace automation should be among them.

Labor shortages materially impede production: nearly one-fifth of firms operating below full capacity cite labor constraints as the cause. Ultimately, a competitive sector will either attract or develop this talent or find ways to automate these needs away. Even more concerning—and addressable—are critical fields like industrial production technologies and industrial engineering, which have experienced respective declines of 23% and 10%, respectively, in graduates from 2018-23 versus a 0.5% decline for engineering programs overall. Generous scholarships can help reverse this trend. As the skilled manufacturing workforce is being rebuilt, Congress should also allow for the issuance of skilled manufacturing visas.

Strategic investment fund

A comprehensive competitiveness strategy must go beyond sectoral fixes. A well-designed strategic investment fund offers one avenue to address systemic financing gaps. The Trump administration, like many of its policies, has expressed multiple objectives for such a fund and a formal proposal is expected to be released soon. These range from the implausible goal of lowering the deficit to establishing a more robust tool of industrial policy or economic statecraft. With the Development Finance Corporation, also up for reauthorization this year, well positioned to play the external role, a lane remains open for a domestic-oriented fund.

Indeed, the fund would be most impactful if it were positioned as an infrastructure bank, helping to address the still considerable barriers to a competitive manufacturing sector that the Biden administration’s infrastructure legislation did not fully address. Some 70% of America’s transmission lines are nearing the end of their useful lives: studies estimate that upgrading America’s energy grid will require $1-2 trillion in investment through 2050.

All that you can’t leave behind

For every potential opportunity the Trump administration has to make meaningful advancements in American manufacturing competitiveness, there are other enablers, such as reform of America’s social safety net, that do not have a viable path - or worse, may be actively degraded over the remainder of his term. In particular, the targeting of America’s universities and research budgets risk profound harm to America’s innovation engine. Assuming Democrats take control of the House in 2027, they will need to right this wrong. A critical act of reparations will be to deliver the research investments authorized by the CHIPS and Science Act that were never appropriated.

America’s manufacturing sector has operated for more than a generation under a capital market that has held it to the highest of standards. As McKinsey notes, in scale-based activities, large US manufacturers average returns of 12 to 14 percent, versus 7 to 9 percent for European companies and 5 to 7 percent for Asian counterparts.” Sectors with higher levels of capital expenditures are rewarded with lower valuations. America must turn its capital discipline into an advantage. The future of manufacturing has always been in scale and now, even more so. It will require that manufacturing capacity look more akin to the platform business models that are so pervasive in the technology sector. That will require private equity “rolling up” capacity, investing in it, and offering it as a service to the most productive use cases; firms like Amazon doing the same thing with its burgeoning robotics capabilities that it has already done with cloud services; and those like Flex leading a new era of outsourcing that is driven less by lower cost and more by continuous improvement and learning across industries.

The trade disruptions of recent weeks underscore the fragility—not inevitability—of American industrial renewal. Policymakers now face a narrow window to take several constructive steps forward. A modern manufacturing strategy will require coordination across a host of policy levers, including trade, capital markets, infrastructure, and education. The Trump administration may yet arrive—intentionally or otherwise—at a combination of policies that has an enduring, positive impact. They’ll need — and, for the country’s sake, deserve — all the help they can get.